What is Smart Risk?

With retirement around the corner, it’s natural to have lots of questions percolating in the back of your mind:

- Will I have enough income in retirement to live the lifestyle I’m used to?

- Will I outlive my savings and retirement investments?

- Should I downsize or should I stay in my current home?

Today’s volatile markets have everyone talking…talking about choices, talking about risk. The low level of interest rates makes it tougher to live off of guaranteed investments, especially when the cost of living seems to keep increasing. According to Statistics Canada, Canadian households are spending an ever-increasing percentage of their total household income on health care. Between 1998 and 2009, out-of-pocket expenditures on health care services and products increased by 2.9% annually1, which is more than what one can earn on a 5 year guaranteed investment certificate (GIC)2. Yet, the volatile markets have people feeling frustrated and confused about how to invest in stocks and bonds or real estate, in order to create a sustainable income in retirement.

These are the same concerns that Victor and Nancy felt when they were introduced to me back in 2007, nearly 10 years ago. They were both in their 60’s, he a retired physician and she a retired teacher, who had saved and invested for many years. Victor had managed the investments across several brokerage accounts for years, but struggled to find a consistent way to move past the emotional fog of investing. He clung to his losing stocks out of fear of selling too soon, tending to “average down” and buy more of the “stories” with which he had grown familiar. He chased high-flying stocks that seemed safe because they were popular, only to regret it when they, too, fell short of expectations. Victor and Nancy both wanted to find a way forward to a financially-secure retirement, but didn’t know how.

The Smart Risk Investing Approach

This changed, however, after the Great Financial Crisis of 2008 – which became the last straw and the catalyst that opened their minds to a new approach. I introduced them to a “Smart Risk Investing” approach, one that is designed to provide a roadmap and clarity, through a sound, dynamic and systematic way to invest.

Smart Risk Investing involves 1. gathering information, 2. weighing the likelihood and impact of each outcome (ie. the probabilities), 3. comparing these outcomes with your tolerance for each, and then 4. taking step-by-step action that increases your chance for successfully reaching your financial purpose and goals. In short, it helps you make reasonable (not emotion-driven) financial decisions that continually stack the odds of success in your favor over the long-term.

I was first introduced to this way of thinking back in the early 2000’s while living and working in New York City. On my second day on the job on the options desk at a major Wall Street investment firm, two planes struck the World Trade Center, and shook the building I was in. The impact of living through and surviving that day created ripple effects and re-shaped how my colleagues and I successfully built investment portfolios designed to provide pension-like income for our wealthy investors in New York.

Years later, in 2008-2009 during the global financial crisis, my purpose was reborn – this time helping Canadians adopt a Smart Risk Investing approach, to help our clients overcome obstacles like volatile markets and emotional investing.

The Smart Risk Revolution

Today, I am leading what I call the Smart Risk Revolution – where my vision is inspiring revolutionary conversations about a new way to think about risk.

My mission is to help investors embrace action – to first think, then act differently when making financial decisions to achieve their goals and purpose.

For example, many of the “universal truths” to investing you believe may actually be outdated as new technology and the abundance of data has challenged the traditional way of investing. For Victor and Nancy, they thought that by having several brokerage accounts holding several mutual funds that they were “well diversified”, when in reality they were not. The global financial crisis exposed their portfolio risks as being much higher and more concentrated than they thought.

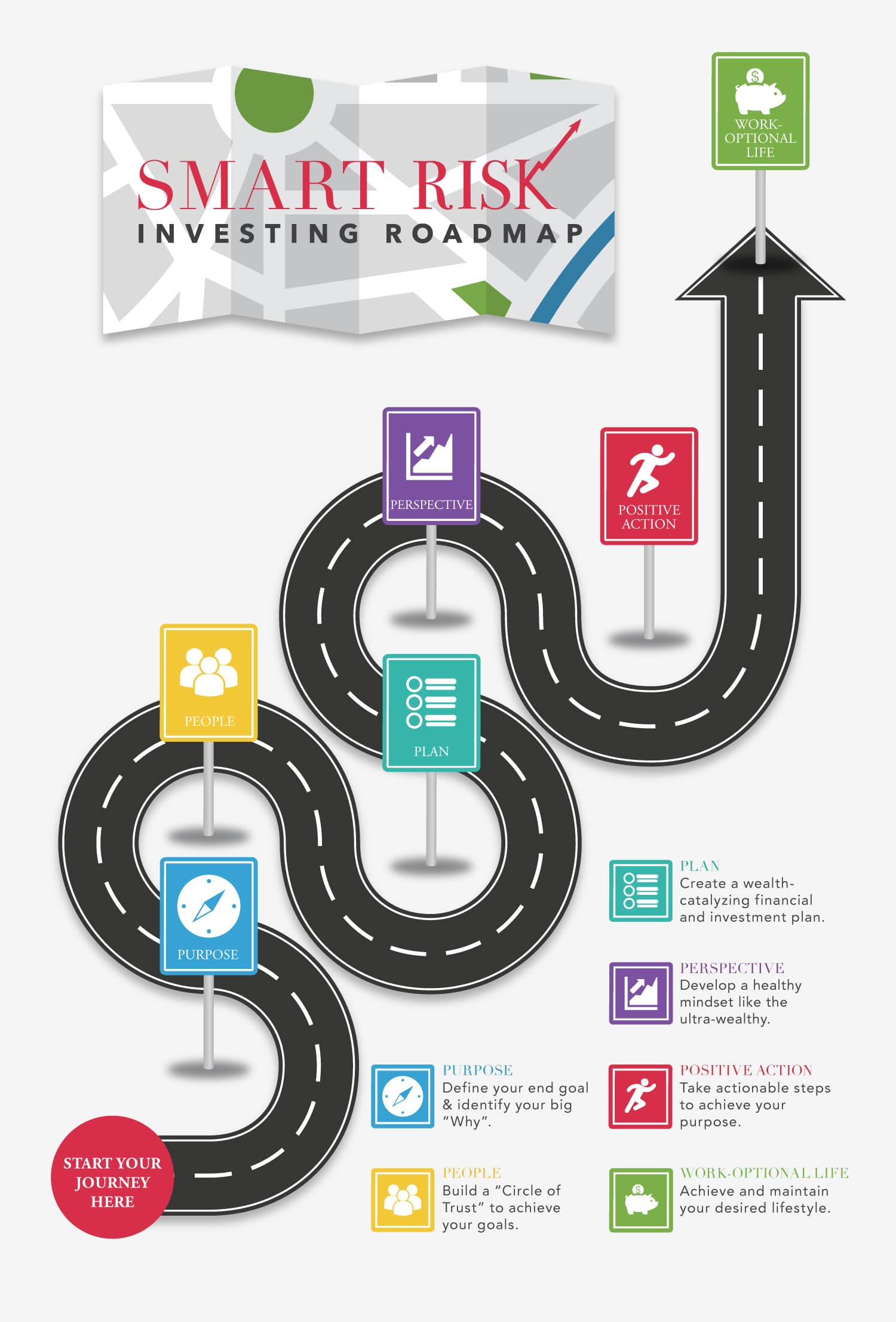

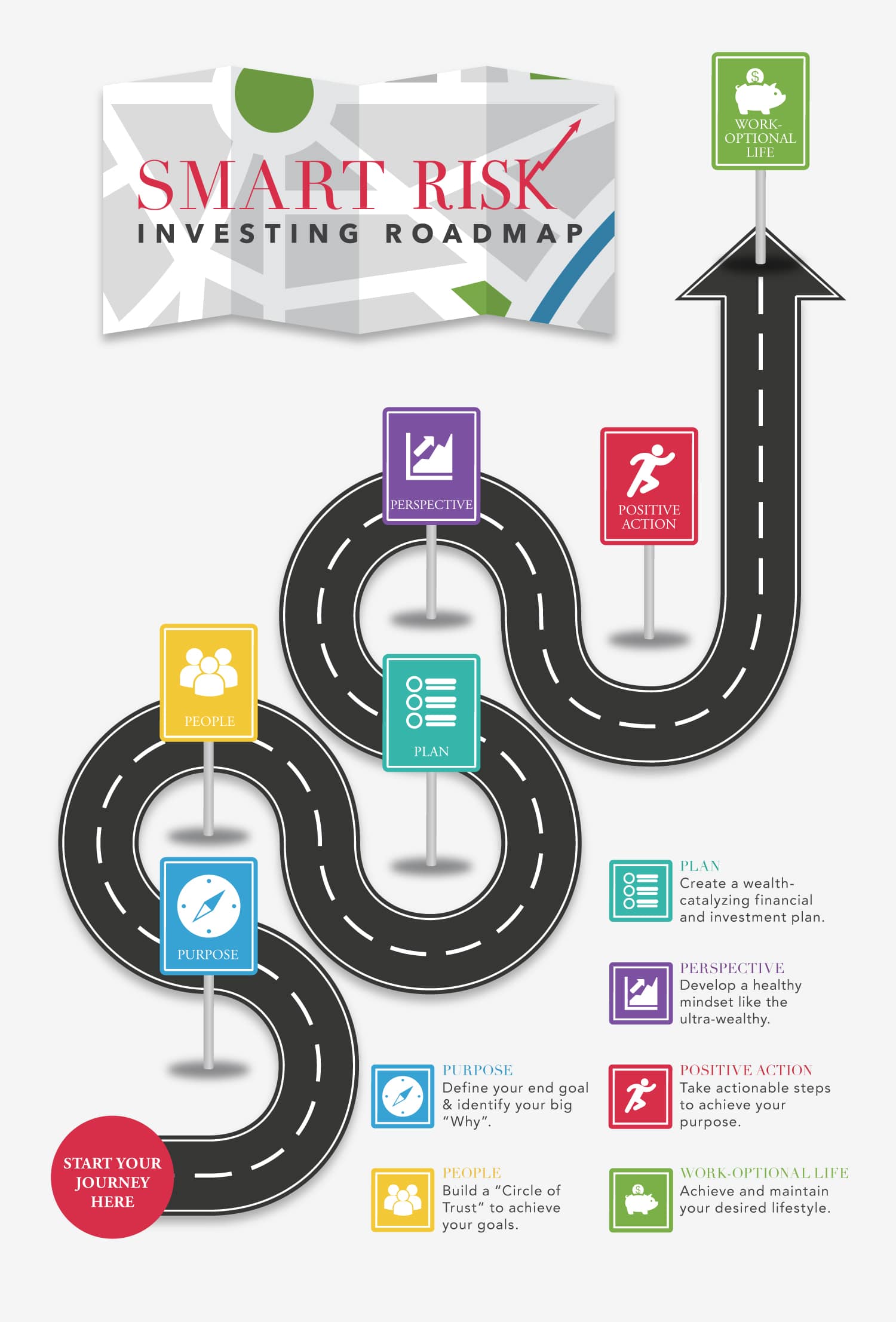

The 5 P’s to Smart Risk Investing

My 15 years of investing for the wealthy has given rise to what I call the Smart Risk Investing Roadmap – a common sense approach made up of five guideposts I call the ‘5 P’s’, to help today’s investors overcome challenges to achieving their financial goals:

It worked for Victor and Nancy, and it can work for you. Read more about Victor and Nancy as well as other examples of this Roadmap in action in the book, “Smart Risk – Invest Like the Wealthy to Achieve a Work-Optional Life”.

As the great Warren Buffet once said, “to invest successfully does not require a stratospheric IQ, unusual business insights, or inside information. What’s needed is a sound, intellectual framework for making decisions, and the ability to keep emotions from corroding the framework”.

Join the conversation at #SMARTRISKREVOLUTION on Twitter.

1. Source: Trends in out-of-pocket health care expenditures in Canada, by household income, 1997 to 2009 report in April 2014, by Statistics Canada.

2. Source: Survey across 5 year Canadian GIC as of February 8, 2016 compared on www.canada.deposits.org